Executive Summary

- Spend policy methodology often receives less attention than the spending rate itself, despite having an equally meaningful impact on the dollars flowing into an institution’s budget.

- While Investment Committees and organizations carefully review the rate annually, the implications and trade-offs of the calculation methodology are often not well understood.

- The key trade-off is between spending stability and long-term endowment growth.

- Each organization should assess its own needs and priorities to ensure the methodology selected aligns with objectives.

- All organizations should be aware that market factors influence each methodology differently.

- Over its 35 years of experience, TIFF has guided clients to understand and select the best spending methodology to meet its objectives.

Rethinking Spend Policy: Why Methodology Matters More Than You Think

Spend policy methodology often receives less attention than the spending rate itself, despite having an equally meaningful impact on the dollars flowing into an institution’s budget. While Investment Committees focus on the rate carefully and annually approve it, they don’t often consider with the same rigor how the spend is calculated, even though the methodology has immense impact on the amount of dollars going into the budget on an annual basis.

Based on various studies, the trailing average market value is the most popular spend methodology.1 However, there are a multitude of other methodologies, each with their own trade-offs. A methodology will perform differently depending on the current economic environment and generally falls along a spectrum of ensuring consistency/growth of spend and protecting the endowment corpus (especially in times of drawdown).

This article provides a framework for institutions to consider their objectives and needs when it comes to their spend, and which methodology might best fit those needs.

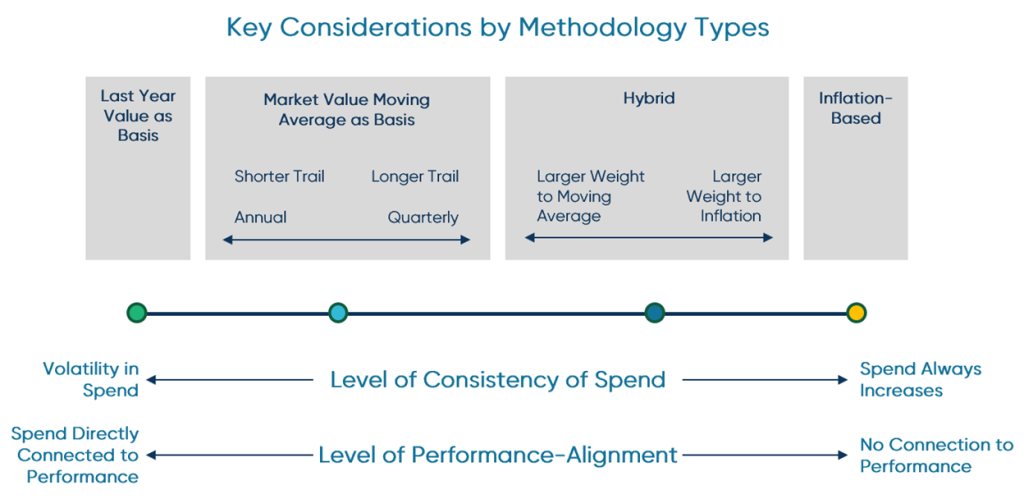

The Three Main Types of Methodologies

Our Spend Policy 101 whitepaper gave an overview of the most commonly used and discussed methodologies. A brief summary is below:

- Endowment Market Value: A predetermined percent of endowment market value, often on a trailing multi-year average basis.

- Inflation-Based: Last year’s spend value increased by inflation, sometimes within a band.

- Hybrid: A combination of market value and inflation.

There are other less common methodologies that we will not discuss in this article.

Trade-offs Among the Methodologies: A Framework for Consideration

Understanding what is important to your institution will help determine the best-aligned spend methodology. These factors should be documented in an institution’s spend policy, to ensure future leaders and fiduciaries understand the choices made. Each organization should assess their organizational preferences and objectives to help determine the best spend policy.

At a high level, institutions must balance institutional needs for consistency of spend value and what best helps build endowment value for the long term. TIFF has outlined conceptually where each methodology falls across these two considerations.

A helpful starting point is assessing the institution’s sensitivity to changes in annual distributions. Organizations that rely heavily on endowment spending to fund their operating budget, or that have limited flexibility in other revenue sources, may prioritize policies that provide greater stability in spending levels. Institutions with more diversified or flexible funding sources may be better positioned to tolerate some variability in annual distributions in order to keep spending more closely aligned with investment performance.

Institutions should also consider their longer-term priorities for the endowment. Policies that prioritize consistency in spending can support budgeting and program stability but may require distributions during periods when the endowment is under pressure (e.g. taking out money during a market drawdown). Approaches that more closely track market performance may introduce short-term variability but can better protect the endowment’s ability to support future generations.

Key Questions for Institutions

To help an institution assess its endowment needs and what spend methodology might be appropriate, TIFF recommends focusing on the following questions:

- How dependent is the institution’s operating budget on endowment spending, and how much variability in annual distributions can it realistically absorb?

- If endowment spending declined meaningfully in a given year (e.g. 10–30%), how would the institution adjust its budget or operations?

- How important is it for annual spending to grow consistently to keep pace with inflation and rising operating costs?

- To what extent should spending be aligned with investment performance to protect the endowment’s long-term purchasing power?

This will help institutions assess their financial flexibility, reliance on endowment funding, need for predictable growth, and priority placed on endowment growth over time.

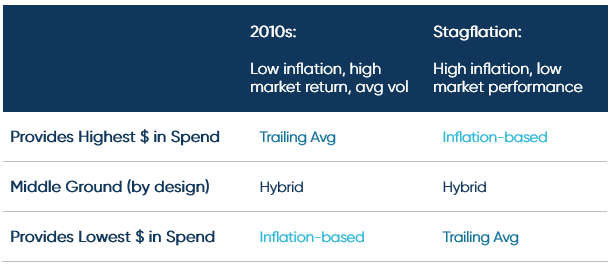

How Market Outlook Impacts Methodology

While it is difficult to predict future market and economic performance, it is important to recognize these factors, though out of any individual’s control, have an impact on the dollars in the institution’s pocket depending on the chosen methodology. While TIFF doesn’t support selecting a spend methodology based on market outlook, institutions should still be aware of the impact market factors have on their choice.

An institution can broadly anticipate each methodology to perform better in a different environment. While there are multiple inputs in the various spend methodologies, there are three key market factors across all of the approaches: (1) inflation, (2) market performance, and (3) market volatility.

A moving average will provide the highest dollars in the withdrawal when market performance is high and inflation is low (e.g. during the 2010s). An inflation-based methodology will produce the highest spend in a stagflation environment, where the spend increases to match inflation as the markets are flat (if not down). Hybrid, as it is a blend, typically ends in the middle of outcomes between market- and inflation-based approaches.

Chart: Case Study of Market Factor Impact on Spending Value

Conclusion

Endowment spending policy is ultimately a reflection of an institution’s financial priorities, risk tolerance, and long-term mission. While the spend rate often receives the most attention, the methodology used to calculate that spending can have an equally meaningful impact on both annual budget support and the preservation of the endowment over time. By thoughtfully considering the trade-offs between spending stability and long-term endowment growth, and by aligning methodology with the institution’s financial structure and objectives, organizations can adopt a policy that supports both present needs and future generations. A well-documented approach ensures that these decisions remain intentional and well understood by future leaders and fiduciaries.

For 35 years, TIFF has helped endowed nonprofits achieve their investment goals to support their missions. One element of that support involves providing strategic governance advice to institutions as they navigate these challenging and “no-right-answer” topics. TIFF helps guide institutions toward the answer that best aligns with their organization’s financial structure, priorities, and mission.

Other Articles by TIFF on Spending Policy

So, You are Considering Changing Your Spend Rate

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance. There is no guarantee that any particular asset allocation or mix of strategies will meet your investment objectives.

The materials are being provided for informational purposes only and constitute neither an offer to sell nor a solicitation of an offer to buy securities. These materials also do not constitute investment, legal or tax advice. Opinions expressed herein are those of TIFF and are not a recommendation to buy or sell any securities.

These materials may contain forward-looking statements relating to future events. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of such terms or other comparable terminology. Although TIFF believes the expectations reflected in the forward-looking statements are reasonable, future results cannot be guaranteed.

The referenced case study is included for illustrative purposes only, and was selected for inclusion based on objective, investment guidelines-based criteria for the purpose of describing the investment processes and analyses that TIFF uses to evaluate such investments.

Footnotes

FY25 Commonfund-NACUBO Study of Endowments, FY25 Commonfund-NBOA Study of Independent Schools.