Executive Summary

- PE exits are reopening. Liquidity is returning after a prolonged slowdown, with 2025 marking a meaningful step forward in overall exit activity.

- Rebound is material but concentrated. Mega-exits have accounted for an outsized share of recovery value, but exit count is also steadily increasing.

- Middle market is showing balanced recovery. Recovery is driven through sustained growth in both exit count and value, suggesting a more durable return of transactions compared to the top end of the market.

- Lower middle market managers are winning through discipline. In this new environment, strong outcomes are being driven less by financial engineering and more by patient realizations, operational execution, and active ownership.

More Than Green Shoots: Exits Return to U.S. Private Equity

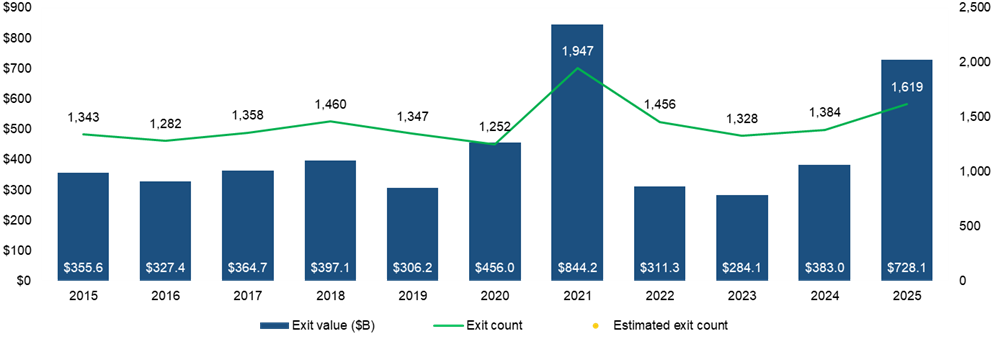

Exit activity is showing encouraging signs of recovery, with 2025 marking a reacceleration in both deal count and value. As buyer-seller expectations begin to converge,1 a greater number of transactions have come to market. In 2025, exit activity showed a meaningful rebound with a 17% increase in total deal count and a 90% increase in total exit value from 2024,2 signaling a reopening of liquidity. Notably, this recovery occurred despite a period of disruption in the second quarter, when market volatility and macro uncertainty, including policy-related events and a government shutdown, temporarily slowed activity.

This return follows a period of dislocation. In 2021, U.S. PE exit activity reached an all-time high. Following COVID-related delays, the surge was driven by exceptionally favorable market conditions like abundant liquidity, strong public valuations, and a backlog of assets ready for sale. As financing tightened and valuation expectations reset, exit activity slowed over the next two years, with many sponsors opting to hold assets rather than transact at lower multiples.

U.S. PE Exit Activity (Q4 2025)

While 2025 marked a meaningful step forward, there is a caveat. According to Pitchbook, 78% of total exit value was accounted for by mega-exits.3 These larger transactions have driven a significant share of the recovery (and of headlines) but, lost in the narrative, there has been a broader, more gradual recovery in the middle market.4

The Middle Market Is Driving a More Durable Exit Recovery

Emerging data points indicate that recovery dynamics are not uniform: Smaller segments of the market are exhibiting more balanced recovery. Activity in the middle market exhibits steady improvement, with exit count and value increasing by 11.6% and 5.6% YoY, respectively.5 Moreover, both exit count and value have increased for the second consecutive year and now surpass pre-pandemic averages for the first time since 2021. This double-digit growth in transaction volume indicates that active deal flow is returning more broadly. As pricing expectations normalize and buyers re-engage, exits in the middle market appear less dependent on episodic liquidity events and more reflective of underlying transaction demand.

U.S. PE Middle-Market Exit Activity (Q4 2025)

Value Creation Over Timing: How the Lower Middle Market (LMM) Is Driving Outcomes

Anecdotal commentary from our own partners provides further perspective on current trends and dynamics in the lower middle market. Their commentary suggests a similar pattern of moderate and nuanced recovery. While overall sentiment remains cautiously optimistic, a few actionable themes emerged from our conversations and research:

- Discipline Over Liquidity: LMM managers remain disciplined on exit timing, with realizations occurring selectively as buyer-seller alignment improves, rather than relying on continuation vehicles or other engineered liquidity solutions.

- Fundamentals Are Driving Outcomes: Returns are increasingly driven by operational execution and earnings growth, with one manager noting that the current environment “rewards firms that generate returns through fundamental business improvement rather than reliance on favorable market conditions.”

- Where Active Ownership Wins: Managers emphasize the ability to drive outcomes through hands-on ownership and sector specialization, with the LMM favoring investors “willing to roll up their sleeves and do the groundwork” in fragmented, recurring-revenue businesses.

A Shift Toward Fundamentals Favors the Lower Middle Market

While remaining cautiously optimistic, LMM managers appear particularly well positioned to capitalize on an exit environment increasingly defined by disciplined underwriting, fundamentals-driven returns, and selective buyer demand. EY reports that 73% of PE firms expect exit activity to increase in 2026, the highest reading since the survey began in 2023, while 79% anticipate a pickup in acquisitions.6 Their expectations are fueled by shifts towards more disciplined entry pricing, more conservative capital structures, and a renewed emphasis on operational value creation.

These shifts are particularly constructive for the lower middle market, where these characteristics are not just cyclical adjustments but long-standing features of the segment. Unlike larger-cap strategies that have historically relied more heavily on multiple expansion and financial engineering, LMM investing has consistently been driven by earnings growth, operational improvement, and hands-on ownership. As returns across private equity become more dependent on these levers, the LMM is structurally aligned with the direction of the market rather than adapting to it.

At the same time, improving acquisition appetite and selective buyer demand reinforce the LMM’s exit pathways. Scaled LMM platforms, particularly those with demonstrated operational progress and defensible unit economics, remain attractive to both strategic buyers and larger sponsors seeking platform expansion. As capital increasingly concentrates around high-quality assets, this dynamic should support consistent exit opportunities for well-positioned LMM companies.

Conclusion

Exit activity in private equity has begun to recover, with 2024 and 2025 marking a clear re-opening of liquidity across the market after a period of below average exit activity. While a few large transactions have grabbed headlines, this masks a more consistent and sustained improvement within the middle market. In particular, the middle market is demonstrating steady gains in transaction activity, supported by a re-engagement of buyers and more disciplined realization behavior. Anecdotal commentary from our lower middle market managers suggests this steady recovery extends to that part of the market as well.

At the same time, the drivers of successful exits are evolving. In contrast to prior cycles that benefited from multiple expansion and favorable financing conditions, current outcomes are increasingly tied to operational performance, earnings growth, and active ownership. This shift favors segments of the market, particularly the lower middle market, that have historically relied on these levers rather than adapting to them.

While near-term exit activity may continue to fluctuate, the evidence suggests that the market is not constrained by a lack of exit opportunities but rather is undergoing a transition toward a more fundamentals-driven environment. As this shift continues, investors positioned with managers capable of executing in this context may be better placed to achieve more consistent liquidity outcomes over time.

The materials are being provided for informational purposes only and constitute neither an offer to sell nor a solicitation of an offer to buy securities. These materials also do not constitute an offer or advertisement of TIFF’s investment advisory services or investment, legal or tax advice. Opinions expressed herein are those of TIFF and are not a recommendation to buy or sell any securities.

These materials may contain forward-looking statements relating to future events. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of such terms or other comparable terminology. Although TIFF believes the expectations reflected in the forward-looking statements are reasonable, future results cannot be guaranteed.

Footnotes

McKinsey & Company. “Global Private Markets Report 2024: Private Markets in a Slower Era.” Feb. 2026.

Pitchbook. “2025 Annual U.S. PE Breakdown – PitchBook.” 14 Jan. 2026.

Pitchbook. “2025 Annual US PE Breakdown – PitchBook.” 14 Jan. 2026.

Bain & Company. “Global Private Equity Report 2019.” 2026.

Pitchbook. “2025 Annual US PE Middle Market Report – PitchBook.” 13 Mar. 2026.

EY. Private Equity Pulse from Q4 2025. 4 Feb. 2026.