Executive Summary

- Hedge funds have consistently delivered through every market cycle, and today the data makes the argument undeniable: now is the time to increase

- Hedge funds outperformed bonds with less risk. From COVID through 2025, hedge funds annualized at 6.1% vs. bonds at 0.9%, with lower volatility. The case for reallocation has never been clearer.

- Alpha is back at levels not seen since the 2000s: Approximately 60% of hedge fund returns over the past five years came from alpha, not beta or luck. Nearly every major strategy beat bonds over the period.

- Public markets are more concentrated than at any point since 1975. Ten stocks now make up 40%+ of the S&P 500. Hedge funds offer the uncorrelated returns and downside protection that a crowded index cannot.

The Enduring Case for Hedge Funds

Change doesn’t announce itself, but looking back, the past five years may come to be seen as the moment hedge funds re-established themselves as an indispensable tool for the modern allocator. The performance in hedge funds in March 2026 during the market downturn is yet another data point. For years, we have been advocating for hedge funds as a core portfolio component, and the data has continued to validate that conviction. Given continued concentration of equity markets, we continue to believe the case for a diversified hedge fund portfolio has never been more important.

Strong Upside Performance and Downside Protection

Hedge funds have demonstrated consistent capital protection through recent periods of market volatility, including COVID, Liberation Day, and the Iran war.

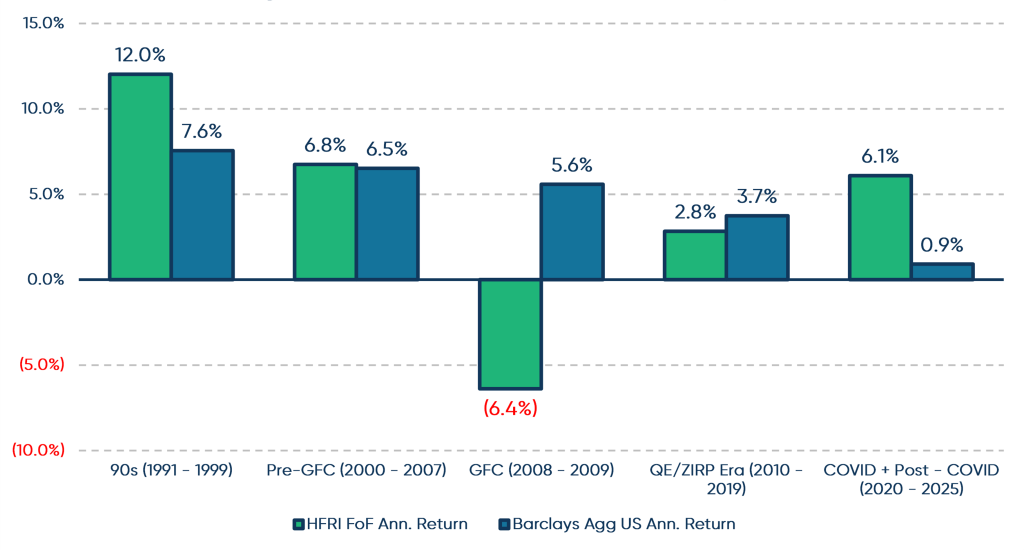

Hedge Funds vs. Bonds Performance Comparison1

Hedge funds continued to benefit from the higher interest rate environment and elevated market dispersion. This drove strong absolute returns in 2025, with the HFRI FoF returning 10.5% for the calendar year against bonds at 7.3%. From COVID through the end of 2025, hedge funds annualized at a healthy 6.1% vs. bonds at 0.9%. This significant dispersion in returns should cause investors to rethink hedge funds’ allocation in a well-rounded portfolio. Simply put: Bonds did not keep pace with inflation while hedge funds delivered real returns with less volatility.

Over this same period, hedge funds have had volatility of 5.6% vs. bonds at 6.0%. This is partially driven by a significant decline in hedge fund volatility to 3.2% over the past 3 years alongside a rise in bond volatility from ~3% to 6%.

What is Driving Hedge Fund Returns? Alpha.

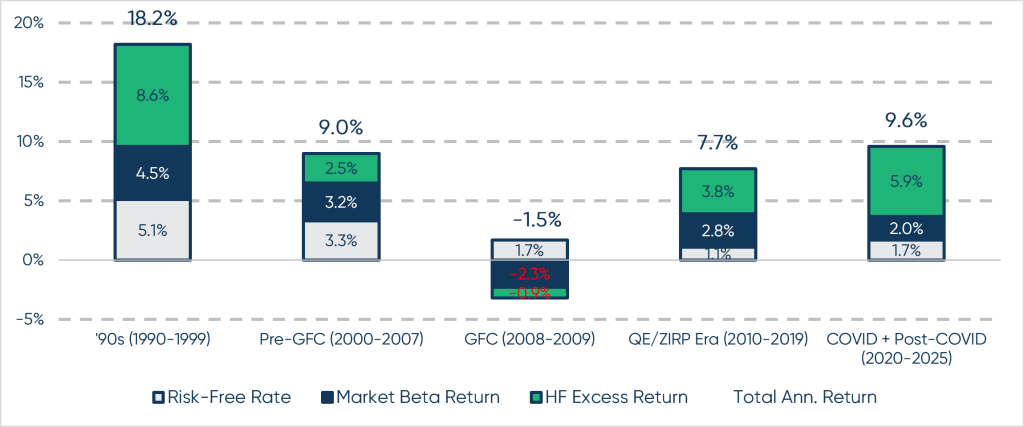

Hedge Fund Performance Breakdown2

Looking at a breakdown of performance across the same period3, we see that not only are hedge funds annualized at their highest rate since the 2000s, but that roughly 60% of performance during the past five years has come from alpha. For those of us with hairlines far back enough to remember, the current period is only surpassed by the last golden age for hedge funds, when rates were a lot higher and markets were far less competitive.

The Need for True Diversification Has Never Been More Important

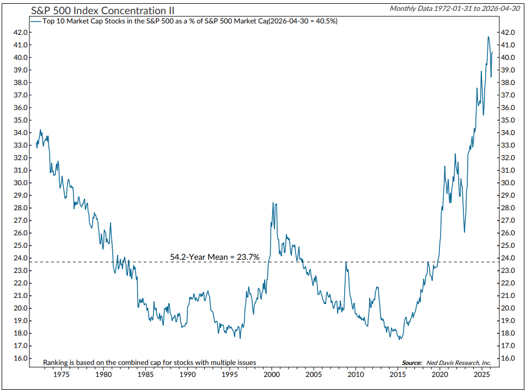

The US Market Is the Most Concentrated It Has Been in Over 50 Years4

Now more than ever, hedge funds should be considered in a diversified portfolio. The chart above highlights the percentage the top 10 stocks within the S&P 500 make up in terms of overall market cap. We are sitting at a whopping 40%+, which is the highest level we have seen since 1975, far surpassing even the levels of the dot-com bubble. The S&P 500 itself no longer meets the SEC’s definition of a “diversified vehicle.” Add to this the upcoming mega-IPOs of SpaceX, Anthropic, and potentially OpenAI, and much of the U.S. market’s fate may rest with a handful of companies.

In these times, hedge funds with uncorrelated return streams and disciplined risk management can help serve a dual role of balancing a portfolio while providing differentiated sources of alpha.

A Stronger Case Than Ever

We understand the stigma against hedge funds is strong among investors who were burned by them in the GFC, but hedge funds as an asset class have evolved over the past decade and provide a much broader range of offerings in today’s market. The macro environment has shifted in hedge funds’ favor, performance has reaccelerated, and disciplined risk management is more valuable than ever in a concentrated, volatile market. Manager selection, strategy diversification, and liquidity management remain the critical variables that separate strong outcomes from poor ones. Navigating exactly that complexity is what we do, so that our clients don’t have to do it alone.

Further Reading

TIFF – Here Comes the Sun – The Rise of Hedge Fund Performance

TIFF – Wind of Change: A Favorable Environment for Hedge Funds

TIFF – Stayin’ Alive: The Importance of Risk Management in a Risky Market

The materials are being provided for informational purposes only and constitute neither an offer to sell nor a solicitation of an offer to buy securities. These materials also do not constitute an offer or advertisement of TIFF’s investment advisory services or investment, legal or tax advice. Opinions expressed herein are those of TIFF and are not a recommendation to buy or sell any securities.

These materials may contain forward-looking statements relating to future events. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of such terms or other comparable terminology. Although TIFF believes the expectations reflected in the forward-looking statements are reasonable, future results cannot be guaranteed.

Footnotes

Source: Factset, HFRI.

Goldman Sachs Prime Research: Generating Alpha, The Hedge Fund Industry Landscape and Outlook for 2026.

Ibid.

NDR Research.