Executive Summary

- Princeton announced it was lowering its endowment expected return from 10.2% to 8%.

- The main reason cited was a slow, decades-long declining return profile, in part due to changing fundamentals of illiquid asset classes (e.g., private equity).

- The impact is reduced future budget support from the endowment, moving Princeton from a decade of strategic growth to a posture of “focus,” “efficiency,” and “substitution rather than addition.”

- This message of budget constraint comes at a time when multiple headwinds are putting pressure on higher education finances. 2025 saw federal university research funding come under attack, along with an endowment tax increase. This is on the heels of multiple years of above-average inflation.

- Is this a big deal? It feels very dramatic! For Princeton, this is a meaningful change and a very real problem that endowed nonprofits face. Princeton’s budget is highly sensitive to changes in the endowment value, as 65% of the budget comes from the annual endowment draw.

- How did Princeton get here? Over the last 25 years, Princeton has made various strategic choices to increase the amount taken from the endowment (i.e., by increasing the spend rate) and used within the budget, which in turn increased Princeton’s budget allocation from the endowment. These choices have been underpinned by an above-average expected endowment return of 10%, which Princeton maintained until this letter.

- Strategic considerations for endowment institutions:

- Acknowledge and understand your endowment dependence

- Understand the spend rate trade-off

- Periodically assess if one’s portfolio aligns with one’s needs

- TIFF has been helping endowed nonprofits navigate these strategic endowment-related topics for 35 years.

From Growth to Focus: Why the Endowment Matters

In Princeton University’s President’s Annual Letter1, President Christopher L. Eisgruber delivered a sober message that Princeton would be moving from a decade of strategic growth to a posture of “focus,” “efficiency,” and “substitution rather than addition.” Underlying this change in tone was a dramatic reduction in Princeton’s endowment expected return, dropping from 10.2% to 8.0%. The stated reason was “changing market fundamentals” in the investment landscape, particularly in illiquid asset classes (e.g., private equity), which faces more competition today than when Princeton began investing in the 1980s. With 65% of Princeton’s budget coming from the endowment, a reduction in expected return means there will be less available capital to flow into the budget in the future. This belt tightening message also comes at a time when higher education is facing a multitude of headwinds, such as shifting federal funding policies, increased endowment tax (for some institutions), and heightened inflation.

The challenge Princeton faces today is an issue all endowed nonprofits face on a regular basis: how to balance maintaining real purchasing power in the endowment while supporting the institution’s mission. However, Princeton has been in a privileged position for decades, with its above-average endowment returns, sustained growth, and ultimately support for the university’s budget.

TIFF took a deeper look at Princeton and what endowed nonprofits can learn from their situation.

Major Contributing Factors to this Predicament

There are three contributing factors related to Princeton’s budget that warranted a letter. All of these factors are interwoven. When the endowment returns are high, the endowment can support an expanding budget while also growing the endowment’s value. However, when expected returns fall, something must adjust–if the spend rate remains the same, the endowment will start to lose purchasing power. At the same time, when such a large percentage of the budget comes from the endowment, any reduction is felt widely.

- High endowment dependency / high sensitivity to changes in endowment value: At 65% endowment reliance, Princeton has the highest dependency in the Ivy League2, and far above similarly-sized peer average of 18.3%.3 While this is a privilege to have freedom from external revenue sources (e.g., tuition), it also makes Princeton’s budget highly sensitive to changes in endowment value.

- High spend rate: The FY25 spend rate was 5.37%, compared to an average peer spend rate of 5.0%.4

- High required expected return: Princeton has maintained an expected return of 10% or higher, compared to the peer average target return of 8.1%.5

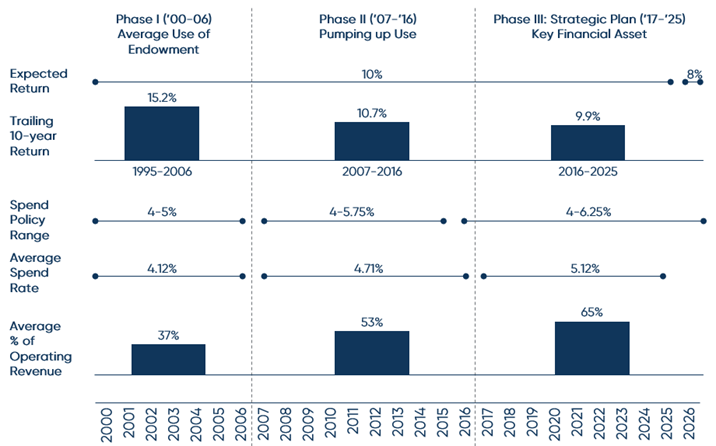

25 Years of Strategic Choices Led Princeton Here

When reading 25 years of Princeton’s annual Report of the Treasurer, it is clear Princeton made strategic decisions to increase the amount taken from the endowment to increase budget support. In the following graphic, I break down 25 years of history into three broad phases. At the end of each phase, Princeton made policy decisions to increase the use of the endowment, which in turn increased the average spend rate and the percentage of operating revenue from the endowment.

Graphic: Summary of Key Princeton Endowment & Budget Related Metrics Over Time

Increased the spend rate policy range by +1.25%, paving the way for larger draws: Princeton voted twice to increase the upper bound of this range, once in 2006 to 5.75% and again in 2015 to 6.25%, with the stated goal of supporting a higher spend rate. In announcing the 2015 increase to 6.25%, Princeton noted that “the Trustees decided that, considering the continued strength of Princeton’s investment program, higher long-term average spending rates could be supported and, indeed, that a higher average rate of spending was needed in order to achieve intergenerational equity, i.e., having endowment spending patterns that balanced the interests of current and future students and faculty.6” Princeton follows a spending policy where the Trustees annually approve a percentage to be taken from the endowment, based on the most recent fiscal year-end value.

Increased endowment draw post-2006: The following 10 years after the first policy change, the average spend rate increased by 14.3%, from 4.1% to 4.7%.

Implemented ambitious strategic plan 2017-2025, pulling more from the endowment: In 2016, Princeton announced an ambitious plan to expand the campus and university offerings.7 It noted at the start of this plan that the university would purposefully draw more from the endowment to support this vision. During this eight year period, the average spend rate increased to 5.12%, up by 8.4% from the prior 10-year average of 4.71%. In addition, during this period, endowment dependency increased in a step-wise fashion. The operating revenue from the endowment for FY14-FY16 was 55%. In the first year of the strategic plan (FY17), endowment support rose to 61% and increased again in FY18 to 65%, where it has generally remained.

Increased endowment dependency by 89%: Over the past 25 years, Princeton’s operating revenue from the endowment increased from 34% in 2000 to 65% in 2025. Each policy increase resulted in a step change in endowment dependency. This has afforded Princeton the ability to implement many of its offerings, such as financial aid packages. However, it also means Princeton has fewer levers to pull in terms of other revenue sources if the endowment doesn’t provide what is expected.

Maintaining of 10% expected return for 25 years: Underpinning all of this financial support is the endowment’s performance and growth. For 25 years, Princeton has maintained its 10% expected return, until 2026. What strikes TIFF as somewhat odd is this consistency. Much has changed in 25 years across all asset classes, and maintaining the same expected return for that length of time is unusual. Perhaps we give Princeton the benefit of the doubt that internally PRINCO had its own varying expectations, and only externally was the 10% noted. However, it is clear that 10% is a key underlying assumption to this endowment-budget relationship, and that assumption did not change.

Three Takeaways from Princeton

- Acknowledge and understand your endowment dependence: An endowment of any size is a gift for a nonprofit, helping to provide financial resiliency and flexibility. However, when dependence on the endowment in one’s budget starts to become significant, it means one’s institution becomes more sensitive to endowment changes. The cushion from diversification of revenue sources decreases as the endowment dependence increases. Having a clear understanding of this dynamic on one’s budget is important.

- Understand the spend rate trade-off: Choosing how much to draw from one’s endowment remains an age-old push and pull between supporting institutional needs today while maintaining purchasing power after inflation. For more details on this trade-off, please refer to TIFF’s piece on how to think about changing of one’s spend rate here.

- Periodically assess if one’s portfolio aligns with needs: Underneath the spend rate and budgetary endowment dependence is the investment portfolio and expected return assumptions. Ensuring that all three of these elements work together in harmony is key to long-term financial health of both the endowment and the institution.

Princeton’s announcement is not just about one university lowering a return assumption. It is a reminder that endowment dependence, spending policy, and institutional specific characteristics must remain aligned, especially in an ever evolving investment landscape. Institutions that proactively revisit these assumptions are better positioned to sustain their missions over the long term.

For 35 years, TIFF has helped endowed nonprofits achieve their investment goals to support their missions. Our work around setting a Strategic Asset Allocation remains grounded in the key issues raised by Princeton’s letter: a portfolio designed to achieve appropriate target returns that support institutional financial needs. As institutions face these questions, TIFF works to help guide the conversation to the answer right for their organization.

The materials are being provided for informational purposes only and constitute neither an offer to sell nor a solicitation of an offer to buy securities. These materials also do not constitute an offer or advertisement of TIFF’s investment advisory services or investment, legal or tax advice. Opinions expressed herein are those of TIFF and are not a recommendation to buy or sell any securities.

These materials may contain forward-looking statements relating to future events. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of such terms or other comparable terminology. Although TIFF believes the expectations reflected in the forward-looking statements are reasonable, future results cannot be guaranteed.

Footnotes

President’s Annual “State of the University” Letter 2026; https://president.princeton.edu/blogs/president%E2%80%99s-annual-%E2%80%9Cstate-university%E2%80%9D-letter-2026-growth-focus.

Spend Policy 101, TIFF Investment Management.

Represents $5B+ segment; FY25 NACUBO-Commonfund Study of Endowments.

ibid.

ibid.

FY2016 Princeton Report of the Treasurer.

Princeton Strategic Framework 2016; https://www.princeton.edu/sites/default/files/documents/2023/05/princetonstrategicplanframework2016.pdf.