Executive Summary

- The rules of corporate behavior in Japan are changing, increasing the investment case for active management and shareholder engagement. Change is being driven by governance reform, pressure from the Tokyo Stock Exchange, the unwinding of cross shareholdings, and demographic pressures.

- The dispersion of speed and change integration is creating an opportunity for active management that can discern the differences between companies and help accelerate them.

- Across public markets, a growing share of equity ownership now sits with passive vehicles, systematic strategies, and shorter horizon investors, which are generally not designed to exercise detailed company-specific influence.

From Cheap Market to Changing Market

The rules of corporate behavior in Japan are changing, increasing the investment case for active management and shareholder engagement. For decades, many Japanese companies prioritized stability, employment, bank relationships, supplier relationships, and other stakeholder objectives over shareholder returns. Cross-shareholding reinforced that system by placing large ownership stakes in the hands of friendly firms that tended to support existing management teams and resisted outside pressure. The result was often inefficient capital allocation, low returns on equity, excess cash, and limited accountability to minority shareholders.

That environment is shifting, with a meaningful increase in shareholder engagement now that change feels feasible. Since the mid-2010s, governance reforms have encouraged stronger board independence, better disclosure, higher returns on capital, more disciplined balance sheets, and the unwinding of cross-shareholdings. These reforms have made shareholder engagement (such as the submission of shareholder proposals by activist investors) more relevant and more effective. They have also helped move Japan from a “cheap market” opportunity to a more targeted, company-by-company opportunity.

The dispersion of speed and change integration is creating an opportunity for active management that can discern the differences between companies and help accelerate them. Japan’s reforms rely heavily on codes, guidelines, incentives, and market pressure rather than hard mandates. This “soft law” approach means companies are moving at different speeds. Some have materially improved governance and capital allocation. Others remain anchored in legacy practices. That gap creates an attractive opportunity for investors who can understand the business, assess management’s willingness to change, and engage constructively where change is possible.

The investment case is reinforced by Japan’s demographics. A large share of Japanese equities are held directly or indirectly by domestic institutions with long-dated retirement obligations, including government-linked pools of capital. As Japan’s population ages, those assets need stronger returns to support retirement obligations. Therefore, governance reform is not just a policy preference; it is tied to a national economic need, often described in Japan as rōgo no anshin — peace of mind in old age. Better capital allocation and stronger corporate returns are aligned with that national priority.

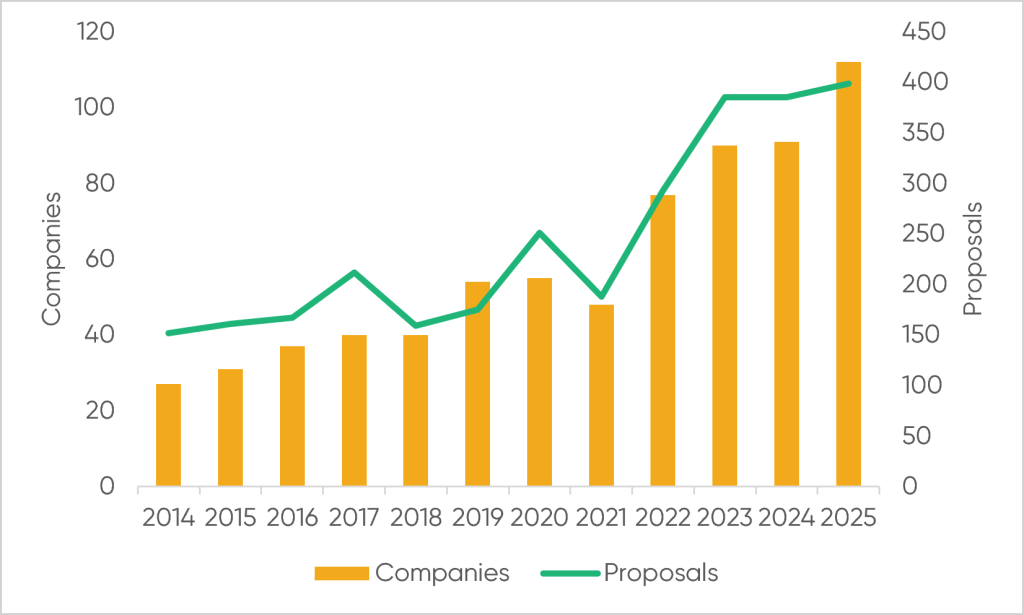

Increasing Number of Shareholder Proposals and Companies Receiving Proposals in Japan1

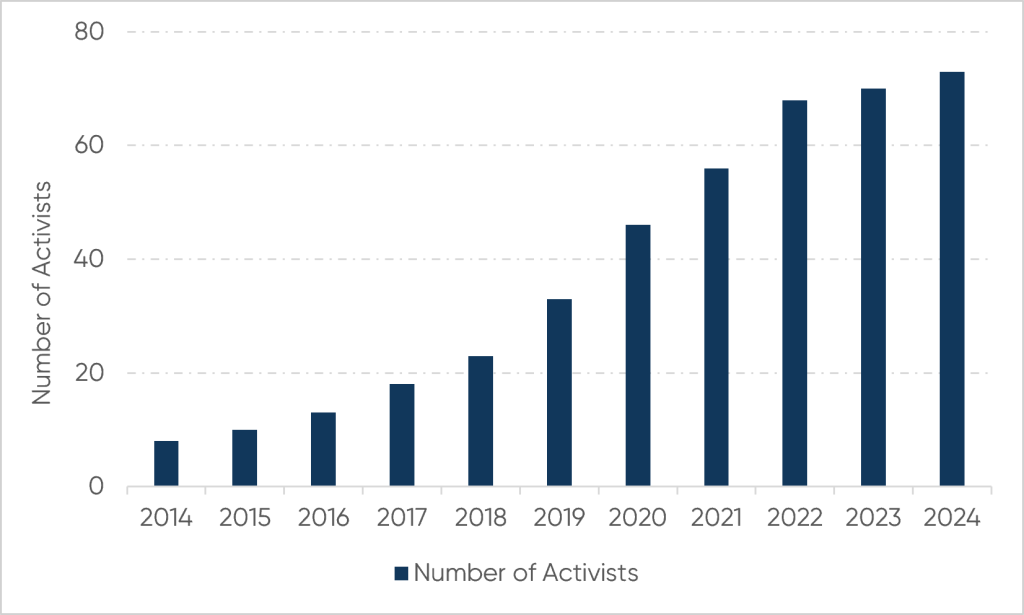

Increasing Number of Activist Investors in Japan2

Why Ownership Alone Is Not Enough

Equity ownership provides two sources of value: an economic claim on future cash flows and a set of control rights, including voting and engagement. Most public market investors focus primarily on the economic claim. In many markets, that has been sufficient. In Japan today, however, the influence component is becoming more valuable as corporate behavior changes and governance reforms create greater dispersion across companies.

At the same time, a growing share of public equities is owned by investors who are not structured to exercise company-specific influence. Passive vehicles provide efficient market exposure, but they are not designed to engage deeply with management teams on strategic or operational issues. Quantitative investors can identify patterns in data, including signals related to governance change, but they are less equipped to assess management credibility, strategic intent, or execution through direct dialogue. Short-horizon investors face different limitations. If a trader is perceived by management to be likely to be out of their stock within weeks or months, they are far less likely to view those shareholders as credible partners on decisions that may take years to unfold.

As a result, ownership and influence are separating in public markets. That creates an advantage for a narrower group of investors: long-term fundamental owners who can combine research, patience, and credible engagement. In Japan, where reform is underway but uneven, that capability can be especially valuable.

What Engaged Investors Can Do

Engagement does not need to mean public activism or confrontation. In many cases, the most effective approach is often behind closed doors with persistent, informed, and tough conversations. A credible investor can help management teams think through capital allocation, balance sheet structure, board composition, asset sales, shareholder returns, and strategic priorities.

The ability to engage matters even when no formal intervention occurs. Management teams know which shareholders are informed, long term, and willing to act if necessary. The presence of those investors alone can influence behavior and encourage greater discipline around major strategic or capital allocation decisions. Engagement also gives investors a deeper understanding of management quality, strategic intent, and execution risk, insights that are often difficult to capture through public information alone.

Conclusion

Japan reflects a broader shift in global public equity markets. As equity ownership increasingly moves toward passive, quantitative, and shorter-horizon investors, fewer shareholders are positioned to influence companies on long term strategic decisions. That dynamic may increase the importance of long-term fundamental investors who engage credibly with management teams on governance, capital allocation, and strategy. Japan is especially compelling because governance reforms and the unwinding of cross-shareholdings are making shareholder influence more effective. For investors, the implication is that differentiated managers may increasingly be those who can combine ownership with constructive engagement. In some markets, shaping outcomes may become as important as identifying value.

The materials are being provided for informational purposes only and constitute neither an offer to sell nor a solicitation of an offer to buy securities. These materials also do not constitute an offer or advertisement of TIFF’s investment advisory services or investment, legal or tax advice. Opinions expressed herein are those of TIFF and are not a recommendation to buy or sell any securities.

These materials may contain forward-looking statements relating to future events. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of such terms or other comparable terminology. Although TIFF believes the expectations reflected in the forward-looking statements are reasonable, future results cannot be guaranteed.

Footnotes

IR Japan, White & Case.

IR Japan.